When an individual files an Ontario bankruptcy he is making a move that will relieve him of a considerable mental burden that has no doubt dragged at his spirit for an uncomfortable stretch. But he’s also signing himself up to honour certain obligations that constitute his side of the bargain.

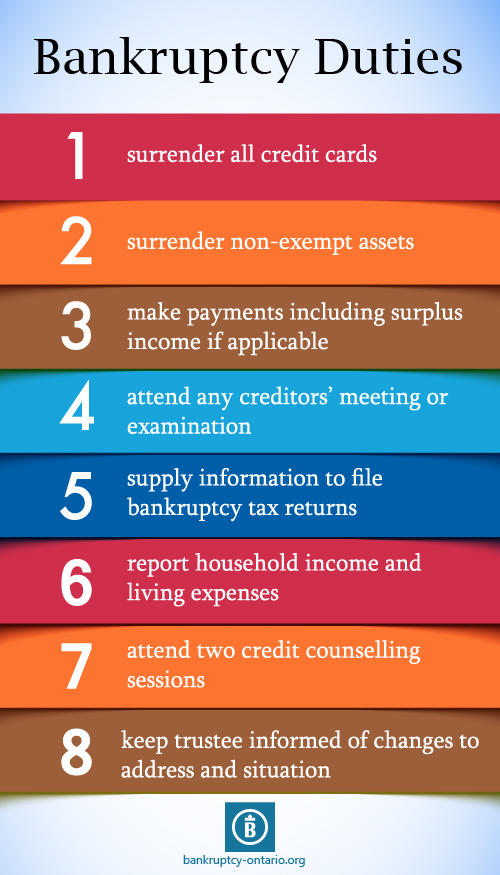

Personal bankruptcy is governed by the Bankruptcy and Insolvency Act for all provinces in Canada, including Ontario. Part of the rules of bankruptcy include the requirement to perform certain duties in order to receive a bankruptcy discharge. Once having filed for bankruptcy, the debtor must:

- surrender all credit cards to the trustee.

- surrender to his trustee all his non-exempt assets. Not all assets are seized in a bankruptcy. Your Ontario bankruptcy trustee will explain what assets you keep and what asset you lose at your initial consultation.

- pay all payments including surplus income payments, if applicable.

- attend a creditors’ meeting, if one is called (this only happens if the Superintendent of Bankruptcy or creditors whose aggregate claims against him total at least 25 percent of proven claims ask for one) or examination under oath with the Office of the Superintendent of Bankruptcy, if it requests such a meeting.

- supply the bankruptcy trustee with information to help file necessary tax returns.

- report household income and living expenses and any change in family situation to the trustee.

- take two credit counselling sessions. The first must be held between 10 and 60 days after the bankruptcy start date; the second must be held within the first 210 days.

- keep the trustee informed at all times of his address and contact information until discharge.

It’s important that all bankrupt individuals cooperate with their trustee and complete these duties in a timely manner throughout the course of their bankruptcy process. This allows their bankruptcy to be discharged as soon as eligible and so you can get you fresh start debt-free.

If you have any questions about your duties and responsibilities, all of this will be explained when meeting with your Ontario Bankruptcy Trustee.

I just have a question that I can’t find an answer to. I filed bankruptcy in 2006 and was discharged in 2007. Included in my bankruptcy was a loan that my father cosigned for. He was responsible for the loan at that time and he paid it off. Now that he has passed away his spouse and her lawyer are harassing me about this money claiming that I owe his estate the money he paid on the loan. I thought that I was discharged from my obligation to the loan through my bankruptcy. I just wondering if I am correct or if my dads spouse can come after me for this money she claims I owe to my dads estate. Any advice you can give me would be greatly appreciated.

Hi Todd. If there is a chance that your father’s estate may take legal action against you, you should consult a lawyer. I can’t give legal advice, but I’ll answer your question in general terms.

If a debt existed at the date of bankruptcy, that debt was discharged in the bankruptcy. It would appear that your father’s spouse is claiming that you had an arrangement with your father that he would repay the co-signed loan, and you would then repay your father at some point. Even if that was true, the loan, either from the bank or from your father, existed at the date of bankruptcy, and therefore was discharged in the bankruptcy.

In addition, your father was a co-signer, so he was also responsible for the loan, which is why he paid it off, so on that basis it would not appear that you are liable.

Again, if this has the potential to become a legal issue, you should seek legal advice.

I was wondering why you are required to surrender all credit cards even if no debt exists on a card. For example, if you have 3 credit cards, but only 2 show a balance owing, do you really have to surrender the 3rd card that has no balance owing? You do not have a debt with that card issuer and are not requesting relief from any debt with them. If you do have to return that card, do you happen to know the underlying reason for this requirement?

Thanks so much for satisfying my curiosity.

Michael

Toronto

HI Michael. I’ll give you two answers:

1. Short answer: It’s the law that you surrender all credit cards. (Section 158 (a.1) of the Bankruptcy & Insolvency Act states that the bankruptcy must “deliver to the trustee, for cancellation, all credit cards issued to and in the possession or control of the bankrupt.”

2. Longer answer: I assume this law exists so that lenders can decide whether or not they want to continue lending to you, even if you are bankrupt. If there was no balance owing on your credit card at the date of bankruptcy and you were not required to surrender the card, the credit card company may not know about your bankruptcy, and therefore they would not have the opportunity to decide whether or not you should be allowed to keep it. The risk for them is that you begin using the card and incur a lot of debt, even though you are bankrupt. By requiring you to surrender all cards, the credit card lenders can then decide if they want to give you another one in the future.